Investing CSE By ABC - An Electrification Future of 'Compute No Enough'

In a post, I mentioned that CSE has The Three Highs:

Price High - Shares up 7% on positive Q4 order wins, closing at $1.36

PE High - 20++. With recognition comes premium.

OrderBook High - CSE Global’s Q4 orders more than double to S$514.7 million on US electrification demand. This brought CSE Global’s total orders secured to a record high of $1 billion for the year.

Some Concerned Citizens commented that CSE may be a handicap due to sufferance of The 3 Highs. We look whether it is hypochondriac to have complaints of a)low margins and b)low dividends, and whether it is an indicator of poor health.

CBA - Conclusion Before Analysis(TLDR)

In short, low margin is indeed a concern but is not that concerning as we move forward, imo.

It is likely the lower margins were Covid-era projects, amongst other factors. Electrification contracts for Amazon and other potential hyper-scaler will enjoy better margins(over time) due to process efficiencies gains, as well as from gaining more recognition for their competencies.

I would expect efficiencies gain, primarily because they are executing projects within their core competencies, as mentioned in the post 'why so special':

[2026-01-05] https://www.investingnote.com/posts/2991793... - CSE Global - What's so special? CSE amazed the amazing people at Amazon that it bought a stake

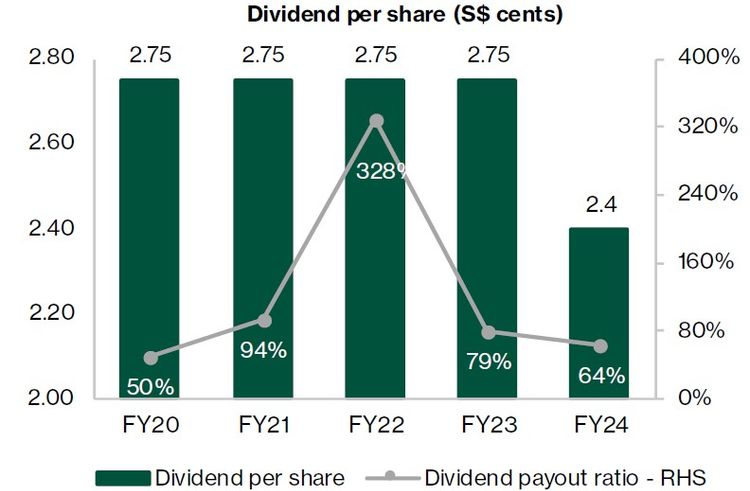

Next, low dividend is a matter of perception as CSE typically targets a dividend payout of around 50% of earnings. For FY2024, the payout ratio was 64% of net profit. In March 2025, the company trimmed its final FY2024 dividend to 1.15 cents (down from 1.5 cents the year prior) basically to front-load the cost to rechannel resources into new growth areas, specifically its expansion into the U.S. electrification market and data centre infrastructure. I would expect it to 're-double' or reward it back in future...

Also, expect it to have lower dividend yield going forward as more analysts and chasers push it to a higher PE. With recognition and certainty, the current yield will always be <3% and PE>20.

Why is CSE Global Profit Margins So Low

It is true that the margins are not high, partly due to legacy projects as well as competition. Currently, one key factor is as managment had explained, they are front loading operational expenses, ahead of the coming demand in 2026++.

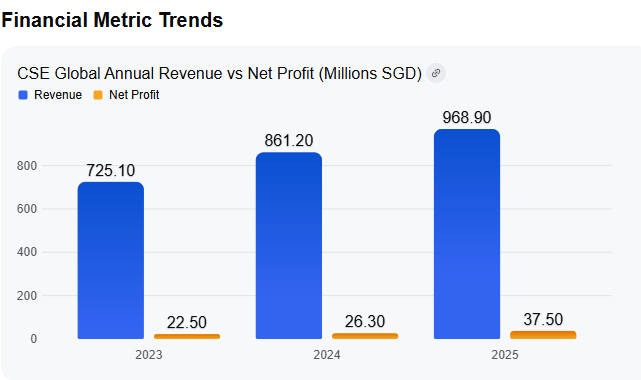

For the 2025 fiscal year, CSE Global reported a net profit margin of approximately 3.9% (based on a net profit of S$37.5 million on S$968.9 million in revenue). While this represents an improvement from previous years, the company's margins are historically low due to its business model as a global systems integrator, which involves high personnel costs and significant "front-loaded" operational investments.

Key Drivers of Low Profit Margins

- Front-Loaded Operational Expenses: In 2025, CSE Global intentionally increased overhead to prepare for large-scale contracts, such as its strategic framework with Amazon. This included hiring additional technical and engineering staff, renting a new 241,000 sq ft facility, and investing in new equipment. These steps are essential for long-term growth but cause near-term margin compression.

- High Personnel and Labor Costs: Operating expenses rose 13.2% to S$211.5 million in FY2025, largely driven by a S$13.8 million increase in personnel costs required to support the expanding electrification business.

- Segment Mix and Project Provisions: Margin performance is often impacted by lower-margin "flow business" or cost provisions in specific sectors. For example, 2025 results included provisions for wastewater projects in the Americas and revenue write-offs in certain automation projects.

- Currency Volatility: With approximately 67% of revenue coming from the Americas, the company is highly exposed to fluctuations in the US dollar. In 2025, revenue growth in some segments was partially offset by the depreciation of the US, Australian, and New Zealand dollars against the Singapore dollar.

Outlook for Margin Improvement

Analysts expect margins to gradually normalize and improve from 2026 onwards as the company's new facilities reach higher utilization levels and revenue from major data centre contracts begins to scale. The record order book of S$709.5 million at the end of 2025 provides strong visibility for this anticipated recovery.

What Is The Margin By Different Division

Generally, the star division is the Electrification segment and I expect it to improve due to recurring Amazon contracts. One reason is that process efficiency can be gained and hence costs reduced over time with repeating jobs.

In FY2025, CSE Global's profit margins varied across its three core segments, influenced by project-specific provisions and strategic expansion costs. The Electrification segment remains the largest revenue driver, though its margins were impacted by investments in data centre capacity.

Segment Profitability (FY2025)The table below summarizes the EBITDA and revenue for each division as of the full-year results reported on 26 February 2026.

| Segment | FY2025 Revenue (S$M) | FY2025 EBITDA (S$M) | EBITDA Margin (%) | Key Driver of Margin |

|---|---|---|---|---|

| Electrification | 507.0 | 45.7 | 9.0% | Lower gross margins from wastewater project reversals; higher labor and facility costs. |

| Communications | 261.7 | ~25.7* | ~9.8% | Impacted by an unfavourable sales mix in the Australia and New Zealand regions. |

| Automation | ~200.2* | ~12.1* | ~6.0% | Pressure from write-offs of plant equipment and technical know-how intangibles. |

*Figures derived from Group FY2025 totals and reported segment growth rates.

Key Segment Insights

- Electrification: While revenue grew 16.6% year-on-year, the EBITDA margin declined slightly from 9.8% in FY2024 to 9.0% in FY2025. This was largely due to S$11.9 million in increased operating costs for expansion and a S$2.4 million revenue reversal in a wastewater project, which was partially offset by a one-off asset disposal gain.

- Communications: This segment saw revenue growth of 12.8%, heavily supported by newly acquired subsidiaries that added S$35.8 million. However, EBITDA growth was modest due to margin pressure from the product mix in international markets.

- Automation: This remains the most volatile segment. In 1H2025, EBITDA for Automation dropped 37.3% year-on-year because of S$5.1 million in intangible asset write-offs. Management noted that while volumes are steady, average contract values have declined.

- Future Outlook (2026): Analysts expect a "Commercial Partnership" related to Amazon to contribute revenue at a ~10% EBITDA margin starting in FY2026, which is expected to support overall margin normalization.

Dividends

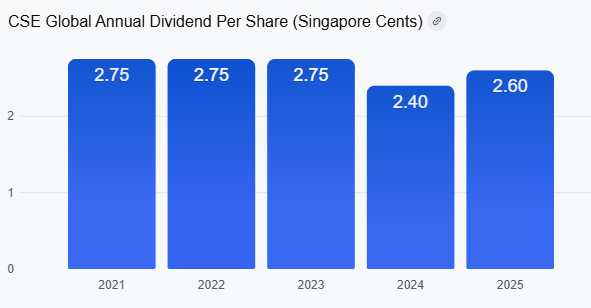

For the 2025 fiscal year, CSE Global actually increased its total dividend by 8.3% to 2.60 Singapore cents per share, up from 2.40 cents in 2024. This increase was supported by a 42.3% surge in net profit to S$37.5 million.

As per the report below, CSE typically targets a dividend payout of around 50% of earnings. For FY2024, total dividends amounted to 2.4 Singapore cents per share, representing 64% of FY2024 net profit.

The perception of a "cut" likely stems from a significant reduction made in early 2025 (for the 2H2024 payout) or fluctuations in the interim 2025 payment.

Reasons for Historical Dividend Fluctuations

- Strategic Repositioning (2024/2025): In March 2025, the company trimmed its final FY2024 dividend to 1.15 cents (down from 1.5 cents the year prior) to rechannel resources into new growth areas, specifically its expansion into the U.S. electrification market and data centre infrastructure.

- Adoption of New Dividend Policy: The Board recently adopted a guidance to payout a minimum of 50% of consolidated net profit. In FY2024, the payout was roughly 64% of net profit, but as the company prioritizes "structural capex growth," it is balancing immediate shareholder returns with the need to fund high-growth projects.

- High Working Capital Needs: In 1H2025, CSE reported a cash outflow from operating activities of S$27.4 million due to higher working capital tied up in major electrification projects. This cash flow pressure can limit the company's ability to raise dividends as aggressively as its earnings growth might suggest.

- Equity Dilution: The company has frequently used a Scrip Dividend Scheme, issuing over 17 million new shares in 2025 alone. This increases the share base, making it more expensive to maintain or grow the dividend amount per share.

Dividend Summary (FY2023 - FY2025)

| Period | Dividend Per Share (SGD) | Change (YoY) | Status |

|---|---|---|---|

| FY2025 Total | 0.0260 | +8.3% | Increased |

| FY2025 Final | 0.0146 | +27.0% | Recommended (Payable June 2026) |

| FY2025 Interim | 0.0114 | -8.8% | Paid Sept 2025 |

| FY2024 Total | 0.0240 | -12.7% | Decreased |

The ABC Of Optimism

A For Amazon

Despite the recent results sell-off due to concerns over AI bubble, and that elevated CAPEX seems aggressive, but it must be viewed in context to the market opportunity. Management highlighted that demand is very strong, and that “Customers really want AWS for core and AI workloads, and we’re monetizing capacity as fast as we can install it.”

Amazon had projected a $200 billion capital expenditure for 2026, significantly higher than the $131.8 billion spent in 2025. The vast majority of this spend is earmarked for AWS to expand data centers, networking, and custom AI chips (Trainium and Graviton). CEO Andy Jassy defended the high spend, stating it is "demand-driven" rather than speculative. Jassy noted that all new AWS capacity is being "absorbed almost as quickly as it becomes available". Management highlighted that AWS backlog surged 40% year-over-year to $244 billion, underscoring strong, long-term, multi-year demand. AWS revenue grew 24% in Q4 2025, the fastest growth in 13 quarters.

B For Agentic Web

Never mind it does not rhyme, but in recent weeks, three events that have not been fully appreciated of the coming convergence of emergence of Agentic Web occured:

- Long running agents

- Markdown has quickly become the lingua franca for agents and AI systems as a whole.

- Agentic Wallets are the first wallet infrastructure built specifically for agents allowing autonomous spending, earning, and trading capabilities.

https://www.coinbase.com/zh-sg/developer-platform/discover/launches/agentic-wallets

C = A+B

Hence, the convergence implies an ABC; where A+B=C and C = Compute No Enough

This theme was previously explored in

[2026-02-09] https://www.investingnote.com/posts/2997974... - Can Mag Fall Elevate CSE?

"not enough compute, hyperscalers are locked into an arms race, ..."

Conclusion

The rise of autonomous agent over the web simply implies current compute is way under-resourced, as agentic workflow works 24x7 and each flow can create an ever virtuous cycle of more agentic 'work'.

Hence, it is elementary to understand that Long Term Bullishness for CSE is as easy as ABC due to this structural long term demand.